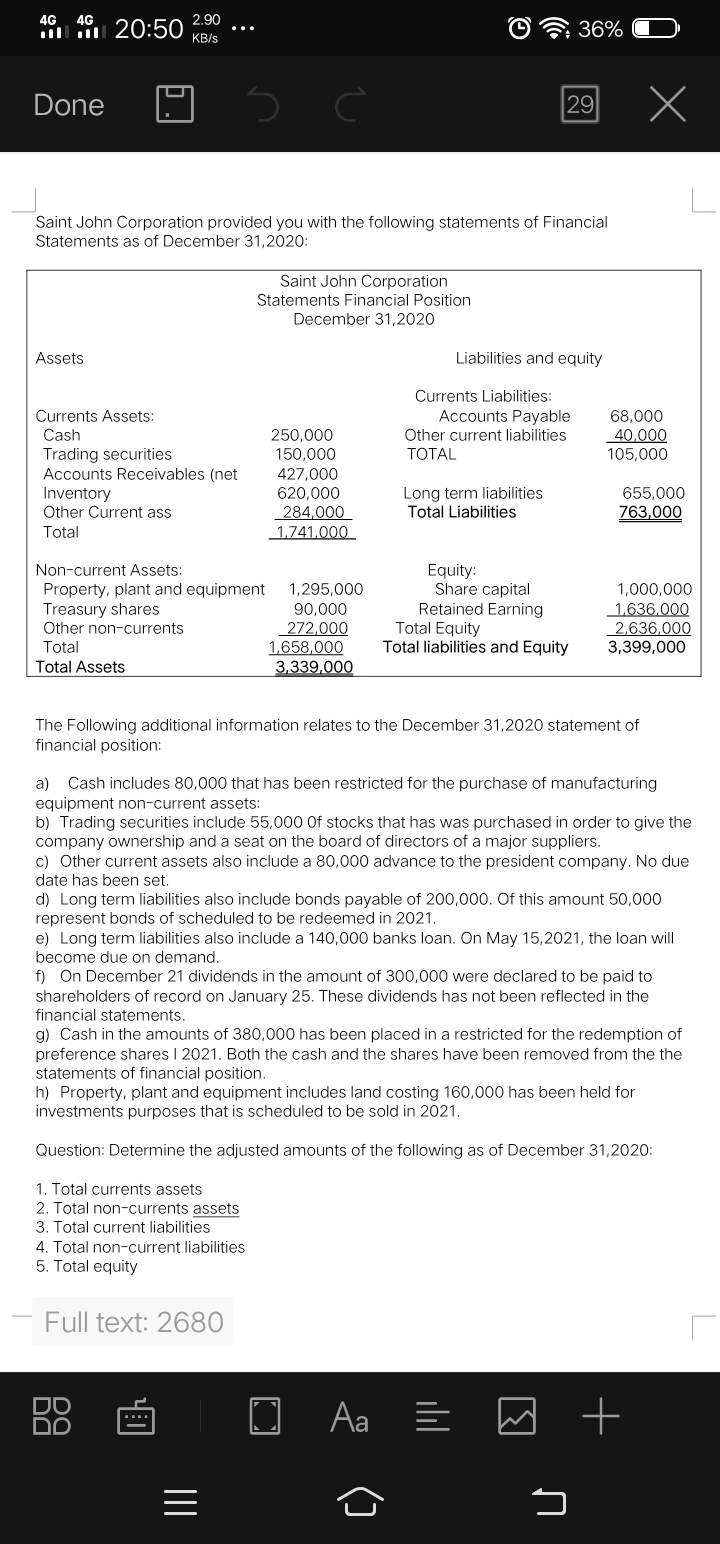

Regarding applying for home financing, you think your most significant decision you make might possibly be anywhere between cost and attract-simply. But not, there’s a new possibility that you might have-not experienced a keen Islamic home loan.

Interest-bearing fund are banned below sharia. Antique mortgage loans are appeal-hit. To help you defeat this issue, Islamic banking companies came up with an item called the Family Get Plan, otherwise HPP. This enables consumers to shop for a home rather than taking right out an interest-affect financing.

In addition, the fresh new Economic Features Settlement Scheme (FSCS) relates to Islamic financial institutions in the same manner it pertains to other British bank

HPP lets a beneficial homebuyer purchasing a property in partnership with new Islamic lender, when you are using lease every month towards the part they don’t really own. The fresh new borrower’s risk in your house develops slowly, over the years.

There is a misconception you to definitely Islamic mortgage loans are only getting Muslims. That isn’t the way it is anyone can submit an application for a keen Islamic home loan based on its issues and needs.

During the early months, banking companies desired homebuyers to get customers of one’s British whenever implementing for a home loan. A changed to help you an even you to definitely non-citizens is now able to and additionally make an application for British mortgage loans, and extremely often do. So it change and relates to other kinds of Islamic financing.

Islamic financial institutions, like other creditors, are controlled by the Monetary Make Power (FCA) and also the Prudential Regulatory Expert (PRA) in britain. Home loan intermediaries you want unique permission throughout the FCA so you can indicates having Islamic mortgage loans. It means one Islamic mortgage loans commonly riskier than traditional mortgage loans.

The fresh FSCS have a tendency to safe monetary tool a consumer has actually purchased from an Islamic financial when your lender collapses

A considerable ratio regarding Islamic banking clients are low-Muslims. Borrowers would like to gain benefit from the special attributes offered from the Islamic mortgage loans. One of many popular functions off Islamic mortgages is the fact of many House Get Arrangements do not best personal loans bad credit Nevada charges a penalty to have early cost.

Foreign traders search assets funding solutions in britain for a few reasons. Islamic mortgages can be a solid type believed BTL property opportunities given that home loan application techniques is 100% online. Some of the antique financial institutions features report-oriented software steps which can be date-consuming and you may inconvenient.

The fresh shrinking musharakah framework is among the most better-known build in the united kingdom, so if you’re taking right out a property Purchase Package, you’ll most likely be utilizing which design. Around it build, the buyer and the Islamic lender purchase the assets mutually, into the visitors adding in initial deposit together with financial providing the others. At that point, the consumer gradually repurchases the house or property from the bank by paying book toward proportion of the home belonging to the financial institution.

The fresh ijara structure is basically the same as diminishing musharakah, whether or not which have one to major difference extent the financial institution leads to the house get is not less by lease paid back. Particularly, say individuals commands property to possess ?two hundred,000; it set-out ?40,000 since put together with harmony out of ?160,000 was provided by the lender. Under an enthusiastic ijarah home loan, you only pay rent toward bank’s area of the family the times. But not, that you don’t make any money towards the getting the ratio of the house that bank owns.

Such as a home loan was normally perhaps not wise when you are to get property which you decide to inhabit, because it forces that promote the house at the bottom of one’s mortgage title to settle the ?160,000 due to the lender.

Lower than a beneficial murabaha framework, brand new Islamic bank often get a house on the borrower’s account and sell an equivalent property during the an increased rate a while later. In the uk, murabaha Islamic mortgage brokers are on the buy-to-let property requests.

Islamic mortgages try flexible and versatile, and can be applied to own family buy plans to own attributes together with BTL resource arrangements.

Total, Islamic mortgages take an upswing, particularly through its unique functions. It is the most useful going back to overseas traders in order to plan its possessions opportunities in the uk. Planning away from Islamic home loan opportunities would-be a significant element of the planning procedure.

Given that a home loan try shielded facing your residence otherwise assets, it may be repossessed unless you keep up the new financial repayments’